The US Securities and Exchange Commission (SEC) on Tuesday charged two Americans and the Malta-based investment advisory firm owned by one of them, Standard Advisory Services Limited, with defrauding clients out of over US$75 million “through undisclosed transactions that benefited themselves and their companies”.

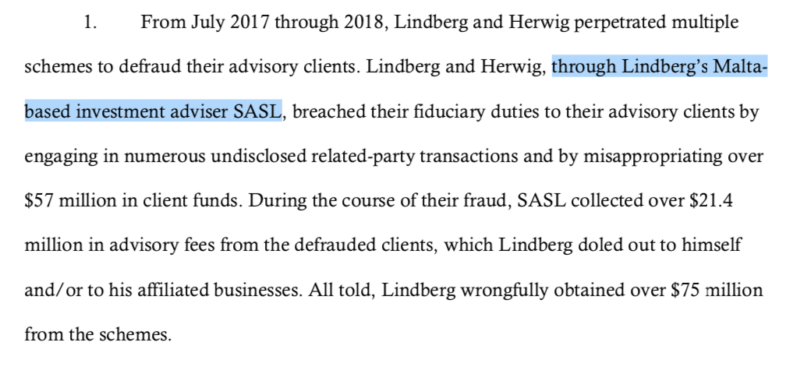

American insurance magnate Gregory Lindberg and Christopher Herwig, through the Malta-based Standard Advisory Services (SASL) owned by Lindberg and the linchpin of the whole operation, stand accused of having fraudulently caused their clients to engage in undisclosed related-party transactions that were, according to the SEC’s charges, far from being in their clients’ best interests.

According to the SEC’s complaint, between July 2017 and 2018, the defendants misappropriated over US$57 million in client funds, with the Malta-based company having collected over US$21.4 million in advisory fees from defrauded clients, money which, according to the SEC, “Lindberg doled out to himself and/or to his affiliated businesses”.

In all, the SEC alleges Lindberg wrongfully obtained over $75 million from the illicit schemes run through the Malta-based business.

In an attempt to conceal the fraud, Lindberg allegedly orchestrated the schemes through complex investment structures and a web of affiliate companies. The funds were allegedly used to pay themselves or to divert the funds to Lindberg’s other businesses.

The SEC alleges that Lindberg, Herwig, and the Maltese SASL, all acting as fiduciaries, “repeatedly recommended and entered into transactions that were not disclosed to and were not in the best interests of their clients”.

While the basic premise of the scheme was simple, the SEC contends that “the mechanics they used to accomplish the fraud were, by design, complex”.

How the schemes worked

By 2017 Lindberg had acquired 100% ownership of four North Carolina insurance companies as well as a reinsurance trust, which gave him control over hundreds of millions of dollars in premiums from policyholders.

Although the funds were meant to have been used to pay policyholders’ insurance claims, “Lindberg treated the funds as his own assets and used the money for any purpose he decided was in his best interest”.

Lindberg instructed his insurance companies to enter into investment advisory services agreements with the Malta-based investment adviser he owned.

From July 2017 through 2018, Lindberg, Herwig, and SASL, in breach of their fiduciary duties, the SEC alleges, “acted in their self-interest and raided their advisory clients’ assets through a series of fraudulent and improper schemes”.

One such scheme saw Lindberg and Herwig advising their clients to enter into “an illogical and complex set of transactions to mask Lindberg’s misappropriation of their funds”.

Specifically, the SEC explains in its complaint that they advised the insurance companies to sell their interests in certain Lindberg-affiliated special purpose vehicles and then to re-purchase what were basically the same investments through a different investment vehicle at a higher price.

“Lindberg pocketed the difference, which was more than $57 million,” the SEC alleges. Between November 2017 and June 2018, Lindberg and Herwig caused the insurance companies to enter into thirteen such transactions.

Lindberg and Herwig used the “fraudulent ‘profits’ to enrich Lindberg and to support his other businesses”, according to the SEC, while the insurance companies’ board members “were left in the dark about Lindberg’s misappropriation”.

An excerpt from the US SEC complaint

In another scheme, Lindberg and Herwig funnelled millions of dollars to Lindberg-owned affiliates by loading the balance sheet of another SASL advisory client, Private Bankers Life & Annuity Co (PLBA), with prohibited and/or sham investments.

Specifically, Lindberg and Herwig allegedly advised PBLA to purchase millions of dollars in securities issued by Lindberg affiliates and hundreds of millions of dollars in illiquid, sham “repurchase agreements” [Repos] issued by Lindberg affiliates.

These related-party transactions violated PBLA’s reinsurance trust agreement, according to the SEC. The Repos, issued by Lindberg-controlled entities “that had no ability or intention to redeem the purportedly short-term liquid investments, violated governing insurance law and PBLA’s investment guidelines and forced PBLA to assume substantial and unnecessary risk”.

In the end, the SEC’s complaint says PBLA “was left holding hundreds of millions of dollars of illiquid, sham Repos while Lindberg and his businesses held cash”.

The four insurance companies’ investment portfolios were heavily compromised, and they were placed into receivership as a result. PBLA itself ended up filing for bankruptcy.

According to the SEC, “Lindberg and Herwig used the proceeds of the fraudulent schemes to pay themselves, to acquire new investment opportunities on behalf of Lindberg, and to transfer large sums of money to Lindberg and his affiliated companies.

“Lindberg disseminated millions of dollars of SASL’s advisory fees to himself and to his affiliated entities that were unrelated to his advisory clients,” the SEC said in its complaint.

They are also accused of spending the illicit profits from the schemes for their own benefit. Herwig received annual salaries ranging from $947,000 to $1.6 million, while Lindberg is accused of having surreptitiously shifted millions of dollars to his personal cash accounts and directed the Malta-based SASL to loan more than $35 million to companies he owned and controlled.

He also directed SASL to issue dividends totalling approximately $12.9 million to a shell parent company he owned.

Lindberg and Herwig declined to testify during the SEC’s investigation, asserting their Fifth Amendment right under the US Constitution against self-incrimination.

‘Massive fraudulent scheme orchestrated for their own benefit’

“We allege a massive fraudulent scheme, involving unique financial structures and various complex investments, orchestrated by the defendants for their own benefit over their advisory clients’ benefit,” Osman Nawaz, the SEC’s Chief of the Division of Enforcement’s Complex Financial Instruments Unit, said on Tuesday.

“Today’s filing demonstrates that the SEC will take action to protect investors from investment advisers who attempt to evade fundamental fiduciary responsibilities.”

The SEC’s complaint was filed in the US District Court for the Middle District of North Carolina and charges Lindberg, Herwig, and the Malta-incorporated Standard Advisory with violating the antifraud provisions of the US Investment Advisers Act of 1940, and seeks disgorgement plus prejudgment interest, penalties and permanent injunctions.

Standard Advisory Services Limited had been issued with a Category 2 Investment Services Licence by the Malta Financial Services Authority. At the end of September 2020, the licence was cancelled after it was surrendered “entirely voluntarily”, according to a statement by the MFSA at the time.

The Malta-based SASL was registered with the SEC as an investment adviser from November 2016 until it withdrew its registration on 1 October 2019.

Lindberg indirectly owned SASL and Lindberg and Herwig were directors of SASL and members of SASL’s investment committee.

Lindberg had also registered a reinsurance company in Malta, Standard Re, in April 2015. It held Class 1 and Class 2 insurance licences issued by the MFSA before its licence was similarly surrendered at the end of 2018.

Another case of Malta in the headlines for the wrong reasons.

Like flies to honey… or is it beetles to dung?

No country has been more ‘fertile’ for corruption than Malta these last 10 years!

Companies only come to Malta to scam, thank you Labor…